In summary, understanding the intricacies of construction bonds and the implications of claims is essential for all stakeholders in the construction industry. These bonds serve as critical tools for risk management, providing security and assurance to project owners while enhancing the credibility of contractors. The claim process, while complex, is designed to protect all parties involved, ensuring that obligations are met and financial losses are mitigated. By navigating the world of construction bonds with informed strategies and thorough documentation, stakeholders can foster a more collaborative and secure construction environment. Ultimately, knowledge is power, and understanding these dynamics can lead to better project outcomes and long-term success in the construction sector.

Weighing the pros and cons of construction bonds reveals that while they offer significant advantages, the associated costs and challenges must be managed effectively. Ultimately, the benefits often outweigh the drawbacks, especially for contractors aiming to establish long-term success in the industry.

The Benefits of Surety Bonds

Obtaining surety bonds comes with numerous benefits that can significantly impact a contractor's business. If you want a deeper dive, check bonded construction projects for examples and key takeaways. One of the primary advantages is increased credibility. Having surety bonds demonstrates to clients and project owners that a contractor is financially responsible and capable of completing projects as promised. This can lead to more business opportunities and potential contracts.

Furthermore, contractors must provide detailed information about their financial stability, including credit history, financial statements, and any previous bonding experiences. Surety companies assess this information to determine the contractor's risk level and decide whether to issue the bond. Contractors with strong financial backgrounds and proven track records are more likely to secure bonds with favorable terms.

Furthermore, contractors must provide detailed information about their financial stability, including credit history, financial statements, and any previous bonding experiences. Surety companies assess this information to determine the contractor's risk level and decide whether to issue the bond. Contractors with strong financial backgrounds and proven track records are more likely to secure bonds with favorable terms. Moreover, contractors should also be aware of the potential for increased premiums if they have a history of claims against their bonds. Surety companies assess risk, and a contractor with a troubled past may face higher costs. Therefore, maintaining a clean record and fulfilling obligations can lead to better bonding rates in the future.

Moreover, contractors should also be aware of the potential for increased premiums if they have a history of claims against their bonds. Surety companies assess risk, and a contractor with a troubled past may face higher costs. Therefore, maintaining a clean record and fulfilling obligations can lead to better bonding rates in the future. Moreover, it’s vital for contractors to negotiate clear terms regarding the distribution of funds. For example, defining when and how payments will be made can prevent potential disputes. Negotiating for a swift payment schedule can also reassure subcontractors and suppliers, which can be a persuasive point in discussions with surety companies.

Moreover, it’s vital for contractors to negotiate clear terms regarding the distribution of funds. For example, defining when and how payments will be made can prevent potential disputes. Negotiating for a swift payment schedule can also reassure subcontractors and suppliers, which can be a persuasive point in discussions with surety companies. Additionally, payment bonds play a crucial role in ensuring subcontractors and suppliers receive payment, which is essential for maintaining good relationships and ensuring the smooth operation of a project. Moreover, contractors may also encounter maintenance bonds, which guarantee that the work will remain free from defects for a specified period after completion, further solidifying trust in the contractor's capabilities.

Additionally, payment bonds play a crucial role in ensuring subcontractors and suppliers receive payment, which is essential for maintaining good relationships and ensuring the smooth operation of a project. Moreover, contractors may also encounter maintenance bonds, which guarantee that the work will remain free from defects for a specified period after completion, further solidifying trust in the contractor's capabilities.Payment Bonds: Ensuring Financial Security

Payment bonds are designed to ensure that subcontractors and suppliers are compensated for their work on a project. When a contractor fails to pay these parties, the project owner can file a claim against the payment bond. This type of bond protects not only the subcontractors but also the project owner, as it prevents potential liens against the property. Payment bonds are particularly important in large projects where multiple subcontractors are involved, as they help maintain cash flow and ensure project continuity.

How long does it take to get approved for a surety bond?

The approval time for a surety bond can vary; it may take anywhere from a few hours to several days, depending on the complexity of your application and your creditworthiness.

The amount of a performance bond typically reflects a percentage of the total contract value, often ranging from 10% to 100%. This percentage varies depending on the project size, complexity, and the contractor's experience. The surety conducts a thorough evaluation of the contractor’s financial stability and past performance before issuing a bond, ensuring that only qualified contractors are bonded. This process helps safeguard project owners and promotes accountability within the construction industry.

The Financial Implications of Construction Bonds

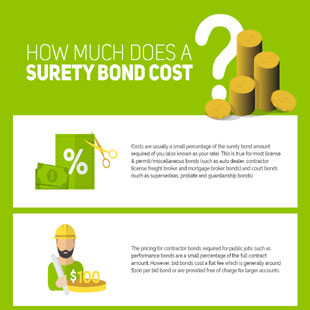

Securing construction bonds comes with financial implications that contractors must consider. The cost of a bond, known as the premium, is typically calculated as a percentage of the bond amount and can vary based on the contractor's financial stability and credit score. Understanding these costs is essential for contractors to budget effectively for their projects.

Once approved, the surety company issues the bond, which typically involves a premium fee based on the bond amount. The premium is usually a percentage of the total bond amount and can vary based on the contractor’s credit history and financial standing. Understanding this cost structure is vital for businesses as they budget for project expenses.