Contractors need to be aware that payment bonds can also protect them from having to pay twice for materials or services rendered. If a supplier or subcontractor does not receive payment from the contractor, they can file a claim against the payment bond. This safety net encourages contractors to maintain open lines of communication and ensure timely payments to all involved parties.

Contractors need to be aware that payment bonds can also protect them from having to pay twice for materials or services rendered. If a supplier or subcontractor does not receive payment from the contractor, they can file a claim against the payment bond. This safety net encourages contractors to maintain open lines of communication and ensure timely payments to all involved parties.What happens if I fail to fulfill my contract obligations?

If a contractor fails to meet their obligations, the project owner can file a claim against the performance bond. The surety will then investigate and may compensate the owner or hire a new contractor to complete the project.

Weighing the pros and cons of securing surety bonds is essential for contractors. While the benefits of financial security and access to larger projects are compelling, contractors must also consider the associated costs and complexities involved in the bonding process. Evaluating these factors in light of individual business circumstances can help contractors make informed decisions about their bonding strategies.

Utilizing project management software can also enhance communication. Many tools offer features that allow for real-time updates and tracking of project timelines. This enables all parties to see where the project stands and what tasks need to be completed. Additionally, having a centralized platform for documentation can prevent miscommunication and keep everyone informed.

The Types of Surety Bonds Subcontractors Should Know

The Types of Surety Bonds Subcontractors Should Know There are several types of surety bonds that subcontractors may encounter, each serving different purposes. The most common types include performance bonds, payment bonds, and bid bonds. A performance bond guarantees that the subcontractor will complete the project according to the contract specifications. If they fail to do so, the surety company will compensate the project owner for any additional costs incurred to complete the work.

General liability insurance protects against claims of bodily injury or property damage that may occur on a job site. Workers’ compensation insurance is essential for covering medical expenses and lost wages for employees injured while working on the project. Builders’ risk insurance, on the other hand, covers damages to the construction site and materials during the building process. Together, these insurance policies provide a comprehensive safety net for contractors and project owners alike.

Evaluating the pros and cons of surety bonds reveals a balanced perspective. While there are costs and challenges associated with obtaining bonds, the benefits—such as increased credibility and access to larger projects—often outweigh the drawbacks. Subcontractors who invest in understanding and securing surety bonds can position themselves for long-term success.

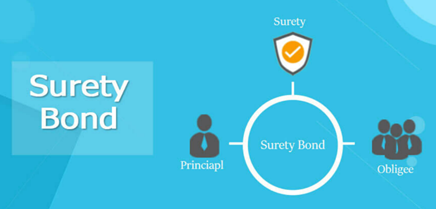

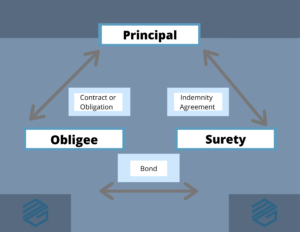

Before diving into savings strategies, it’s crucial to understand what surety bonds entail. Here is more info in regards to performance and payment bonds check out our own page. A surety bond is an agreement among three parties: the principal (the contractor), the obligee (the project owner), and the surety (the bonding company). The surety provides a financial guarantee to the obligee that the principal will comply with the terms of the contract. The importance of these bonds cannot be overstated, as they not only assure project owners of a contractor's reliability but also play a significant role in enhancing the contractor's reputation. This foundation sets the stage for exploring how contractors can effectively save on these critical financial instruments.

How can contractors improve their chances of obtaining bonds?

Contractors can improve their chances of obtaining bonds by maintaining good credit, having clear financial records, and building strong relationships with surety companies. Additionally, providing evidence of past successes can enhance their credibility.

Leveraging Surety Bonds for Business Growth

Leveraging Surety Bonds for Business Growth Surety bonds can serve as a powerful tool for subcontractors looking to expand their business. By obtaining bonds, subcontractors can bid on larger projects that require bonding, which can significantly increase their revenue potential. This ability to take on more substantial contracts can lead to a more diverse portfolio and improved financial stability.

Delving deeper, it’s vital to recognize that construction bonds and insurance are not merely interchangeable terms. Each offers a specific type of protection and serves different parties involved in a construction project. For instance, a bond guarantees that a contractor will fulfill their contractual obligations, while insurance provides coverage against unforeseen risks and liabilities. By understanding these nuances, stakeholders can make informed decisions that mitigate risks while ensuring that their projects run smoothly.

While there are challenges associated with securing surety bonds, the long-term benefits often outweigh the costs. Subcontractors who invest in their knowledge of surety bonds and maintain strong relationships with surety companies will find themselves better equipped to navigate the competitive landscape of the construction industry. Ultimately, embracing the advantages of surety bonds can pave the way for substantial growth, stability, and success in a subcontractor's career.

While there are challenges associated with securing surety bonds, the long-term benefits often outweigh the costs. Subcontractors who invest in their knowledge of surety bonds and maintain strong relationships with surety companies will find themselves better equipped to navigate the competitive landscape of the construction industry. Ultimately, embracing the advantages of surety bonds can pave the way for substantial growth, stability, and success in a subcontractor's career.