Common Misconceptions about Surety Bonds

Despite their benefits, there are several common misconceptions about surety bonds that can deter businesses from utilizing them. For more perspective, see Axcess Surety Underwriting Approach for examples and key takeaways. One prevalent myth is that surety bonds are only necessary for large corporations or contractors. In reality, any business seeking to establish credibility and secure contracts can benefit from surety bonds, regardless of size.

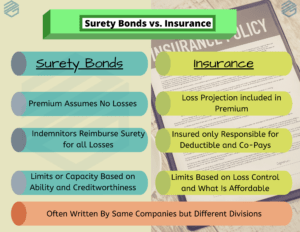

Legal Aspects of Bonds and Insurance

Both construction bonds and insurance are subject to legal regulations that can vary by state or region. Understanding these legal frameworks is essential for contractors to ensure compliance and avoid potential pitfalls. For example, some states may require specific types of insurance or bonds for certain projects, especially public works.

Moreover, construction insurance can be tailored to meet the specific needs of a project. Contractors can select policies and coverage limits that align with the risks associated with their work. This customization ensures that they are adequately protected without overpaying for unnecessary coverage.

Moreover, construction insurance can be tailored to meet the specific needs of a project. Contractors can select policies and coverage limits that align with the risks associated with their work. This customization ensures that they are adequately protected without overpaying for unnecessary coverage. Next, businesses must complete a bond application, which typically includes details about the project or obligation that requires the bond. This aspect of the application process is crucial because the surety needs to understand the scope and nature of the work involved. Moreover, some sureties may require collateral, particularly from businesses with limited credit history, which can be an important consideration for cash management.

Next, businesses must complete a bond application, which typically includes details about the project or obligation that requires the bond. This aspect of the application process is crucial because the surety needs to understand the scope and nature of the work involved. Moreover, some sureties may require collateral, particularly from businesses with limited credit history, which can be an important consideration for cash management. When embarking on a construction project, whether it's a small renovation or a large-scale development, understanding the financial safeguards available is crucial. Many contractors and project owners often find themselves grappling with the differences between construction bonds and insurance. While both serve to protect financial interests, they operate under different principles and provide unique benefits. In this discussion, we will explore these two essential tools, unveiling their distinct roles and how they can be utilized effectively in the construction industry.

When embarking on a construction project, whether it's a small renovation or a large-scale development, understanding the financial safeguards available is crucial. Many contractors and project owners often find themselves grappling with the differences between construction bonds and insurance. While both serve to protect financial interests, they operate under different principles and provide unique benefits. In this discussion, we will explore these two essential tools, unveiling their distinct roles and how they can be utilized effectively in the construction industry.As you navigate the complexities of construction financing, remember to assess your specific needs, consult with professionals, and regularly review your options to ensure optimal protection. By effectively leveraging both construction bonds and insurance, you can safeguard your interests and achieve successful project outcomes. This knowledge not only empowers you as a contractor or project owner but also strengthens the integrity of the construction industry as a whole.

The benefits of construction insurance are manifold. Firstly, it provides peace of mind, knowing that financial protections are in place against various risks. This can be especially important for contractors who may face significant liabilities if accidents or damages occur. Additionally, having insurance can enhance a contractor's credibility, as clients often prefer working with insured professionals.

How Surety Bonds Work

How Surety Bonds Work The process of obtaining a surety bond begins with a thorough application where the contractor must provide detailed financial information. Sureties assess the contractor's creditworthiness, business experience, and financial stability to determine eligibility. This assessment is crucial, as it helps the surety gauge the risk involved in issuing the bond.

The Significance of Credit Scores in Surety Bond Approval

The Significance of Credit Scores in Surety Bond Approval The role of credit scores in securing surety bonds cannot be understated. Surety companies assess the risk associated with bonding an individual or business, and one of the primary indicators of that risk is the credit score. A higher credit score typically indicates a lower risk for the surety company. Consequently, individuals and businesses with strong credit ratings are often offered better terms and lower premiums. This relationship makes understanding and managing your credit score crucial for anyone interested in obtaining a surety bond.

In addition to enhancing balance sheets, surety bonds can improve cash flow management. Since they assure clients of project completion, businesses may find it easier to secure financing options, leading to better liquidity. This is particularly important for small businesses that often operate on tight budgets and depend on timely cash flow for operational continuity.

Bond Type

Application

Typical Use Case

Performance Bond

Guarantees completion of a project

Construction projects

Payment Bond

Ensures payment to subcontractors

Construction and service contracts

Bid Bond

Guarantees contract signing if bid is accepted

Project bidding

License Bond

Ensures compliance with regulations

Various industries

Permit Bond

Secures permits for businesses

Construction and development